Source: Adobe Stock. Ozempic by Novo Nordisk

Eli Lilly has furthered its lead over weight-loss rival Novo Nordisk after a landmark $1 trillion market capitalisation.

The first pharmaceutical company to reach such a milestone, Lilly’s success helped lift the benchmark S&P 500 Health Care Index to unfounded yearly highs. The firm’s rally comes at the behest of new U.S. government initiatives, causing the sector to strengthen.

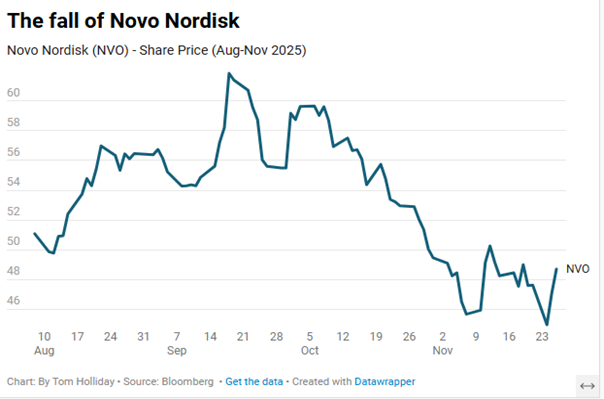

The outlier in the sector comes in the form of Danish rival, Novo Nordisk, as it continues its slide, circling yearly lows following a weakening demand for its core product offering an addition to consecutive guidance cuts on its yearly financials.

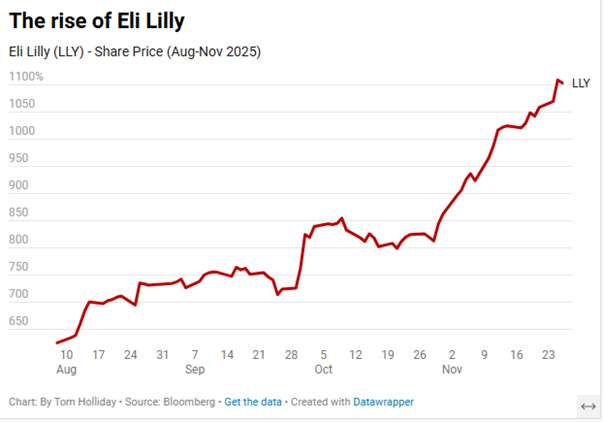

Lilly closed the day up 0.8 per cent, prolonging a four-month rally that has seen its share price rise above $1,100 from an original $625 in early August. This uptake has positioned Lilly at forefront of not only the popular GLP-1 weight-loss market, but more broadly of the entire U.S. healthcare sector.

An analyst at J.P. Morgan, who requested to remain anonymous, cited a “large and still underpenetrated obesity opportunity” for the firm, which should position Lilly for significant growth in 2026.

Formerly a two-party race, the other GLP-1 contender, the Danish Novo Nordisk, has diverged greatly in recent months, experiencing a dissimilar level of growth compared to its U.S counterpart.

Originally the lesser to Novo as Europe’s then most valuable company, Lilly entered the month of August trading at yearly lows, a period that marked greater weakness unanimously across U.S. healthcare equities. At the same time, the S&P 500 Health Care Index was circling yearly lows, reverberating a dullish investment attitude across the sector.

Those conditions did not prevail. Promising third-quarter earnings, catalysed by growing demand for Lilly’s obesity medication’s Mounjaro and Zepbound, aided in reversing sentiment. Revenues began to climb sharply, provoking the firm to raise its full year revenue and earnings guidance.

The rally continued into the fourth quarter, supported by a November agreement announced by the Trump administration to expand access to GLP-1 medications through government programmes including Medicaid and Medicare. Analysts have declared a positive outlook in light of the deal, with illuding to the offset of pricing pressure through increased volumes.

“We increasingly see the recent agreement with the Trump administration expanding government access to obesity medicines as a net positive, with incremental volumes more than offsetting prices,” the JP Morgan analyst said.

According to data from FinViz, GLP-1 medications now dominate amongst Lilly’s sales mix, with Mounjaro and Zepbound bearing responsibility for more than 50 per cent of total revenues in the first nine-months of 2025.

By late November, Lilly was up near 40 per cent year-on-year.

The same period has proved more of a challenge for Novo Nordisk, despite the prevailing strength seen in biotech and healthcare equities.

The Danish drugmaker has slowing growth in demand for its staple obesity treatments Wegovy and Ozempic, notably in the U.S. market. In late July, the company downgraded its full year guidance, lowering expected sales growth and prompting analysts to take similar action with their earnings expectations.

Rajesh Kumar, an analyst at HSBC said that while hopes for Novo’s Alzheimer’s programme had never formed a significant part of his valuation, the trials still represented an “attractive risk reward catalyst”. He added that “the timing of any potential re rating now remains uncertain”.

The pressure stepped up for the firm following a disappointing third-quarter earnings report, exhibiting a sharp decline in operating profits following a restructuring charge. Analysts resultantly cut earnings outlooks for both this year and the next.

Michael Leuchten, an analyst at Jefferies said that although expectation for a positive Alzheimer’s trial readout was “not high”, the possibility of success had likely kept investors from completely withdrawing their positions. Proceeding the failure of the trial, he said it was “unlikely investors will rush back in Novo shares in the near term”.

In attempt to rejuvenate demand, in mid-November, Novo announced that it would reduce the monthly price of injectable Wegovy for cash paying US consumers. Additionally, it pledged to prioritise the development of an oral version of the drug for the U.S. market. Novo said the move is anticipated to have a “low single digit negative impact” on global sales growth next year.

The divergence has been particularly notable given the bullishness of the wider biotechnology sector, which has continued to pursue yearly highs.

As Lilly consolidates its position at the forefront of the GLP-1 market, the challenge for it’s Danish rival is whether it can recover demand and restore investor confidence in the coming months.

Comments