Source: Wikimedia Commons. Map of Venezuela featuring the Orinoco Belt.

Over a week ago, US Treasury Secretary Scott Bessent announced the decision of the Trump administration to fully roll-back a seven-year embargo on Venezuelan crude oil, following the capture of former president Nicolás Maduro, marking a significant turning point in US foreign policy.

This was confirmed via a statement from the US Energy Department citing the intention to ‘enable the transport and sale of Venezuelan crude oil and products to global markets’.

With an estimated 303 billion barrels in reserve, Venezuela is home to the largest proven crude oil deposits, representing around 17 per cent of the world’s total, bringing new meaning to Trump’s 2025 mantra of “drill, baby, drill” as well as his expansive use of executive authority.

Audacity withstanding, the move has left markets unsure, with the average oil investor remaining indecisive to such a policy shock, now beholden to dynamics of the ‘Trump Trade’.

“These foreign policy gymnastics are upending assumptions about oil supply and leaving markets scrambling to adjust,” said Argus Media in a recent statement, leaving many wondering about the implications for oil markets now that Venezuela is a likely participant.

What happened to the price of oil?

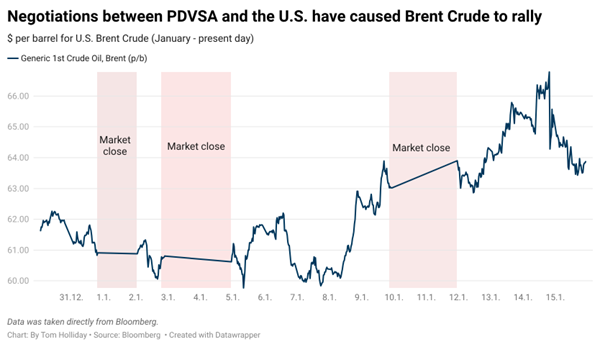

Following the capture of Maduro, U.S. Brent Crude (Brent) endured a limited price reaction with levels holding just below $62 per barrel as investors chose to hold their positions.

‘Price reaction was muted given ample global crude supply,’ said analysts at Argus Media.

A muted initial response to a new front of US economic positioning, the discrepancies in Brent pricing began on 8th January in which negotiations between the U.S. and PDVSA (Petroleos de Venezuela), the state-owned oil company of Venezuela began.

In anticipation of a new-found, energy-focused relationship between Trump and Venezuela’s new head of state, former vice president and US cooperative Delcy Rodriguez, investors bolstered their positions in Brent, with the per barrel price enduring almost a weeklong rally, reaching highs of $66.78.

The rally proved short lived with the market readjusting toward median levels of $63 in the early hours of January 15th.

‘Despite having the world’s largest proven crude oil reserves, Venezuela produced only 0.8 per cent of total global crude oil in 2023,’ said the USs Energy Information Administration (EIA).

Equivalent to 742,000 barrels per day, this represents a 70 per cent cumulative decline from their production levels 2013.

A rate of production which is ‘unlikely to move the needle in a meaningful way’, said Argus Media analysts, speaking to stabilisation of the market.

The intentions of Trump to bring Venezuelan oil to the shores of the U.S remain under cautious scepticism by investors.

Where is the long-term value of Venezuelan oil?

For the bullish investor and the refineries, they bet on, the long-term reintroduction of Venezuelan oil to the US has been viewed positively.

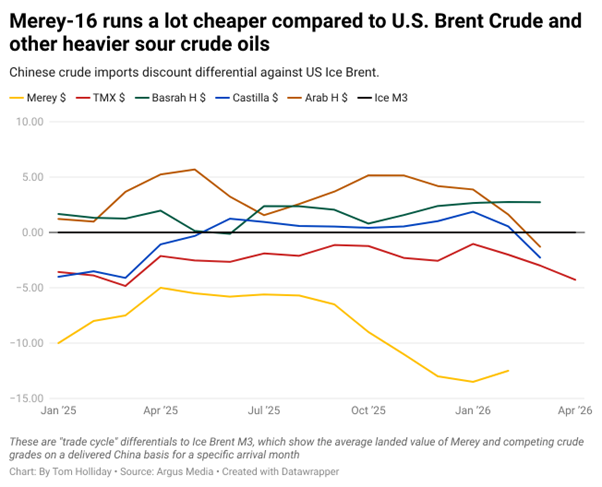

Beginning in 2017, when Trump placed sanctions upon the PDVSA, prohibiting the exchange of natural resources between the two nations, Venezuela’s sour heavy crude, Merey-16, became limited in supply.

This is ‘a quality of oil they have been sorely lacking,’ said Argus Media, addressing the global shortage of Venezuela’s particular kind of crude.

A fact which no longer appears the case with the recent US intervention potentially returning 500,000 – 600,000 barrels a day of heavy sour crude to global markets, the firm estimates.

This supports a more favourable outlook for US coastal refineries who, since the imposition of US sanctions, have turned to the likes of Canada and the Middle East for their supply of heavy sour crude, often at a higher cost.

According to EIA analysis, Merey-16’s liberation will enable the shorter-haul imports at a cheaper price for the US.

A prospect which the market reflected in tighter price differentials with the spread between Merey-16 and US Brent reducing by around $1, signalling an increase in value for the sour heavy crude and a scheduled recovery for the constrained Venezuelan oil sector.

Are markets confident in this ‘Trump Trade’?

Following the apprehension of Maduro, Venezuela’s defaulted debt instruments rose almost 30 per cent, serving modest gains to eager investors.

In default since 2017, Venezuela’s government bonds jumped 42 cents on the dollar. A 33-cent increase from the value prior to the operation. Bonds issued by PDVSA, the state oil company also exhibited gains, rising from 26 cents to 33 cents.

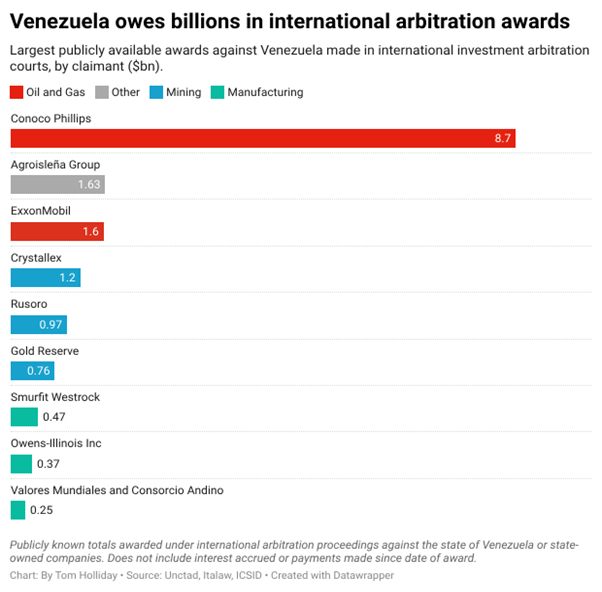

The price Venezuelan issued bonds collapsed in 2017 following the US sanctions, raising the lower bounds of Venezuela’s estimated debt level to around $150bn. A level greater than twice the size of the country’s economy.

This includes more than $20bn in claims tied to international arbitration awards that had their assets expropriated by the Venezuelan government including US firms ConocoPhllips and ExxonMobil.

The bond rally suggests investors are reevaluating political risk, but prices persist in reflecting Venezuela’s large debt pile and lack of credible oil infrastructure, breathing further uncertainty into the longevity of US policy.

Comments